As the coronavirus continues to spread globally and airlines cancel most flights in and out of China, investors are probably wondering – should airlines be avoided for the near future? Not necessarily. We view it as a buying opportunity. The economic repercussions of this global health emergency will no doubt have a big impact on airlines and tourism, but we expect the industry to return back to normal levels after the virus is contained.

If investors are seeking a precedent to compare to the recent coronavirus, they need only look back 10 years, when the H1N1 Swine flu made it the U.S. via Mexico. An estimated half a million people died as a result of the virus, 12,000 in the U.S. alone. Major U.S. carriers were impacted, with Delta Air Lines reporting between $125 million and $150 million in lost revenue, according to a note from Credit Suisse. But the virus was relatively short-lived, and the industry promptly recovered.

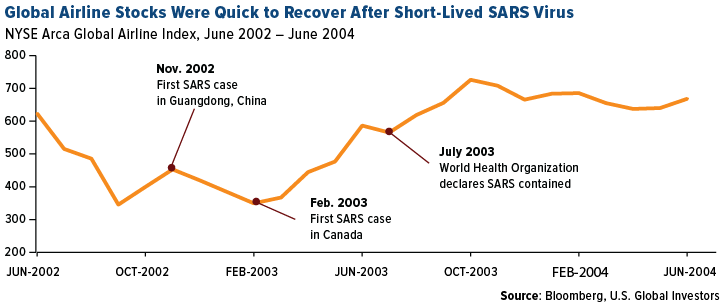

Before that, in 2003, was the SARS epidemic. Air traffic to China fell by nearly half year-over-year in the second quarter of that year, which may have had a negative impact on airline earnings. Credit Suisse points out it’s hard to estimate SARS’ impact on airlines since there was also the Iraq War, not to mention a weak macro environment at the time.

Airlines, as measured by the NYSE Arca Global Airline Index, were quick to recover once the threat of SARS dissipated, and carriers were citing normalization of trends, including capacity growth, in the second half of 2003. However, The International Air Transport Authority (IATA) estimated that the 2003 SARS outbreak cost Asia Pacific carriers $6 billion in revenue. Analysts already forecast that the economic hit from coronavirus will be far greater than that of SARS, given the higher death toll and quarantine of the world’s second largest economy.

Chinese Travel Demand Remains Strong

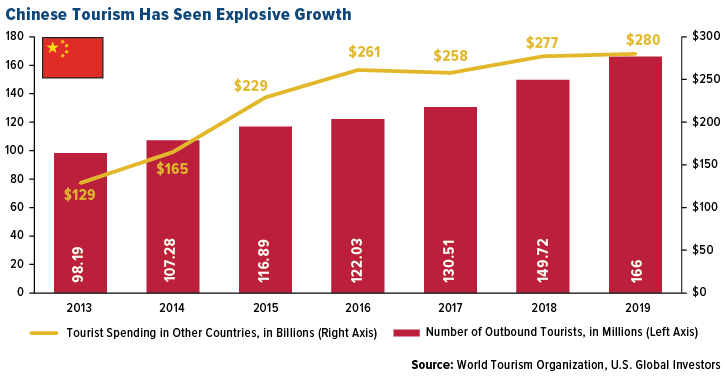

To be clear, we see incredible opportunity in the travel sector. Chinese tourism has seen explosive growth over the years as incomes have risen. At the end of 2018, the size of China’s middle class stood at approximately 400 million, larger than the entire U.S. population. The number of outbound Chinese tourists in 2019 was an estimated 166 million, while travel spending topped a whopping $280 billion.

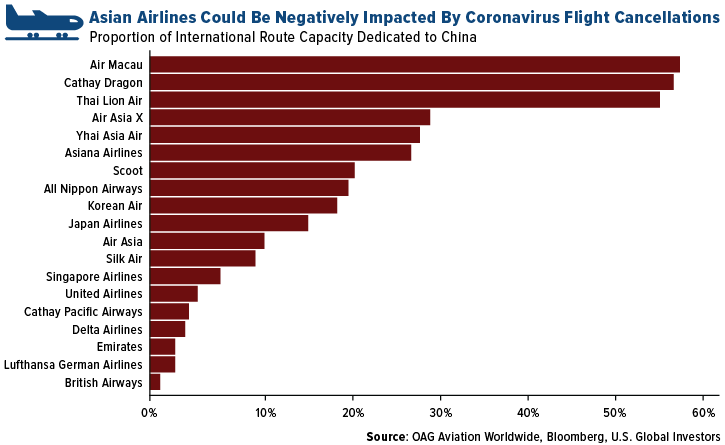

Airlines globally have been cancelling services in and out of China over fears of the virus spreading further, which will likely hurt earnings due to the lost revenue. According to data from OAG Aviation Worldwide, Air Macau and Cathay Dragon have the biggest proportion of their international route capacity exposed to the mainland China market.

Fortunately for the U.S. Global Jets ETF (JETS), the only airline-focused ETF on the market, it has a relatively small allocation to carriers with exposure to the Chinese market. Of those displayed above, JETS only holds positions in the following: Japan Airlines, United Airlines and Delta Air Lines. United and Delta are top holdings in the fund, however, those airlines only have a small portion of international route capacity dedicated to China.

JETS invests in the global airline sector, including airport operators and manufacturers, but focuses on the U.S. airline market with the top four holdings the largest four domestic carriers. Sanghamitra Saha, writing for Zacks, recently commented that owning airlines through an ETF approach “takes care of company-specific concentration risks as one company’s strength [could] compensate for another company’s weakness.” Saha adds that “it is better to tap the ETF option for the U.S. airlines industry as stock performance have been uneven in the past month (February).”

Airlines Are Still Cheap

As pointed out by a recent Barron’s article, airline stocks in the S&P 1500 have the lowest price-to-earnings (P/E) ratio of any subsector on the market. The U.S. Global Jets ETF (JETS) has a P/E ratio of 9.49, much cheaper than the wider S&P 1500 Index with a ratio of 22.42, as of February 12.

In December 2019, of course long before the virus outbreak, the IATA released a bullish forecast for 2020. The organization expects the global airline industry to produce a net profit of $29.3 billion for the year, up from an expected profit of $25.9 million in 2019. The IATA also forecasts return on invested capital of 6 percent and net profit margin of 3.4 percent, both figures up from the 2019 estimates.

If you agree and expect the air travel trend to rebound and continue to grow, now might be a buying opportunity to enter the space before stocks potentially recover from the coronavirus outbreak.

Learn more about the JETS ETF and how you can invest in a variety of airlines, airport operators, manufacturers and more – click here.

The price-to-earnings ratio is the ratio for valuing a company that measures its current share price relative to its per-share earnings. It is also known as the price multiple or the earnings multiple.

The S&P 1500 includes all stocks in the S&P 500, S&P 400 and S&P 600, and covers approximately 90 percent of the marketing capitalization of U.S. stocks.

The NYSE Arca Airline Index is a modified equal- dollar weighted index designed to measure the performance of highly capitalized and liquid international airline companies. The Index tracks the price performance of selected local market stocks or American depository receipts (ADRs) of major U.S. and overseas airlines.

Sign up for our monthly recap of the airline sector here.